Is College Worth It? How Median ROI Hides a Harsh Reality

I want to start Part 3 with something that's been on my mind: the power of example, and the danger of leaving things unsaid.

I sometimes sense a hesitance among many to talk about the downsides of college. The worry is that acknowledging the risks might discourage people from pursuing it.

I had a conversation recently with a mentor whose work I really admire. She questioned whether it made sense to talk about downsides at all. Wouldn't it be better to focus on the opportunity?

Here's what I told her.

For people on the South Side of Chicago you can't ignore the downsides, because it's something they live and breathe every day whether you acknowledge them or not.

Do you think students don't see their friends go off to college with great fanfare and slink home one year, two years later because they couldn't afford it?

Do you think they don't know about the conversations their brothers or sisters or cousins or friends are having with their parents about what is and is not possible?

Of course they do. In many ways, they know this better than you ever could.

So the only thing you actually accomplish by ignoring the downsides is establishing that you are either oblivious to the realities they deal with every day — or too scared or ill-equipped to grapple with them.

In my case, the person who did more than anyone else to get me to the University of Chicago was my Army recruiter.

He didn't just sell me a dream. He showed me how the Army could solve the problems I had to solve that day, how I could leverage it to get what I wanted ( remember those online courses I took in Iraq? That was his idea) and he was able to clearly articulate the challenges and setbacks I might face in doing it this way.

That's why I trusted him. That's why his advice worked.

My point is this: we have to be as well-versed in talking about the downsides of going to college as we are in talking about the upsides. Not to discourage anyone. Because that's what credibility requires.

Which leads us to the other side of the median.

What "Median" Actually Means (and what it doesn't)

When researchers talk about college ROI, they almost always use medians. Median earnings. Median debt. Median time to repayment.

There's a good reason for this. Medians are stable. They're not thrown off by outliers. When someone says "the median college graduate earns X dollars," that's a reasonable summary of a typical outcome.

However, the median isn't a promise. It's not a floor. It's the middle of a distribution — and distributions have tails.

At every school, 25% of people who entered earn at or below the 25th percentile (P25). Some finished. Some didn't. We'll unpack that composition later — but either way, a quarter of entrants land there.

The question we're gonna unpack today is: what happens to them?

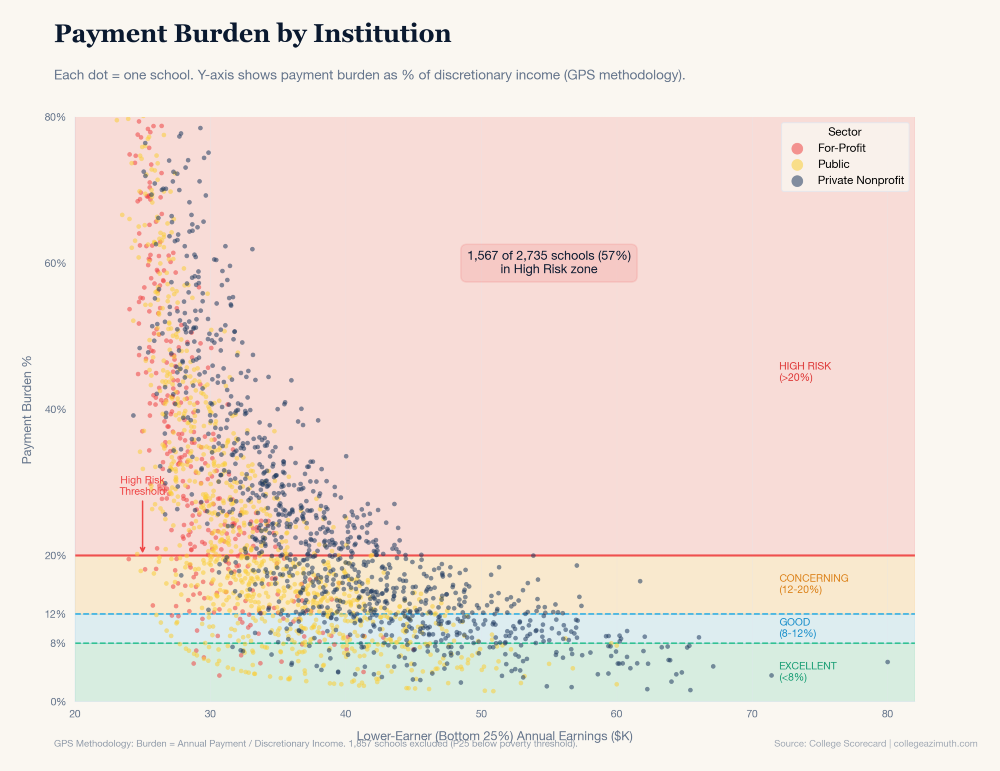

The reality of the bottom 25 Percent.

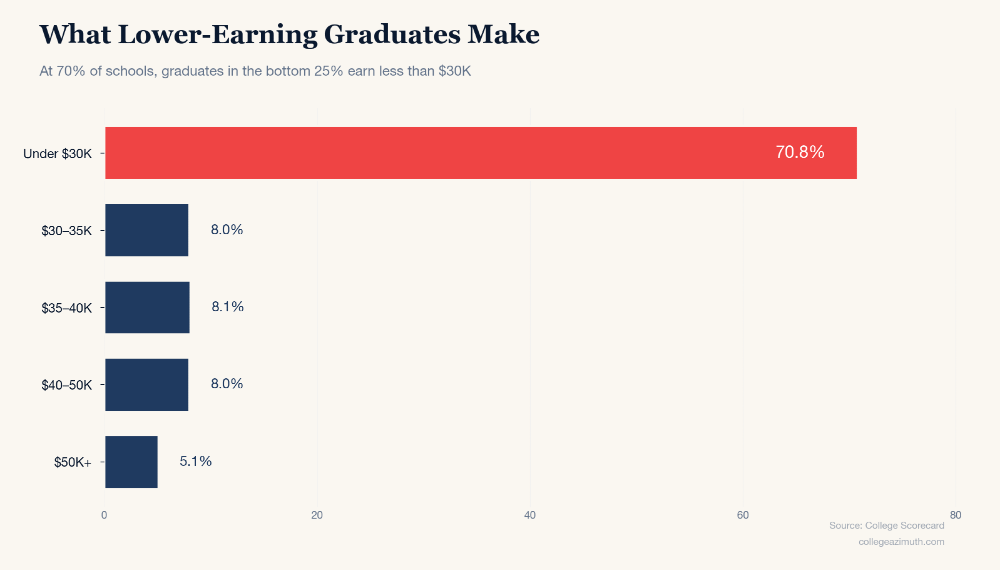

Here's what the earnings look like for the bottom 25 percent (P25) at universities across the country:

At 70% of schools, P25 earnings are below 30,000 dollars a year.

To put that in context: under our affordability framework, 31,300 dollars is the threshold for "discretionary income" — the point below which you're covering basic needs and have nothing left over.[1]

At 72.5% of schools, P25 graduates earn below that threshold. They have zero discretionary income under any reasonable definition.

For them, "break-even" isn't delayed. It's undefined. You can't pay down debt from income you don't have.

| P25 Earnings | % of Schools | Implication |

|---|---|---|

| Under 30K | 70.8% | No discretionary income |

| 30-35K | 8.0% | 25-100+ year break-even |

| 35-50K | 16.1% | 10-25 year break-even |

| 50K+ | 5.1% | Reasonable break-even |

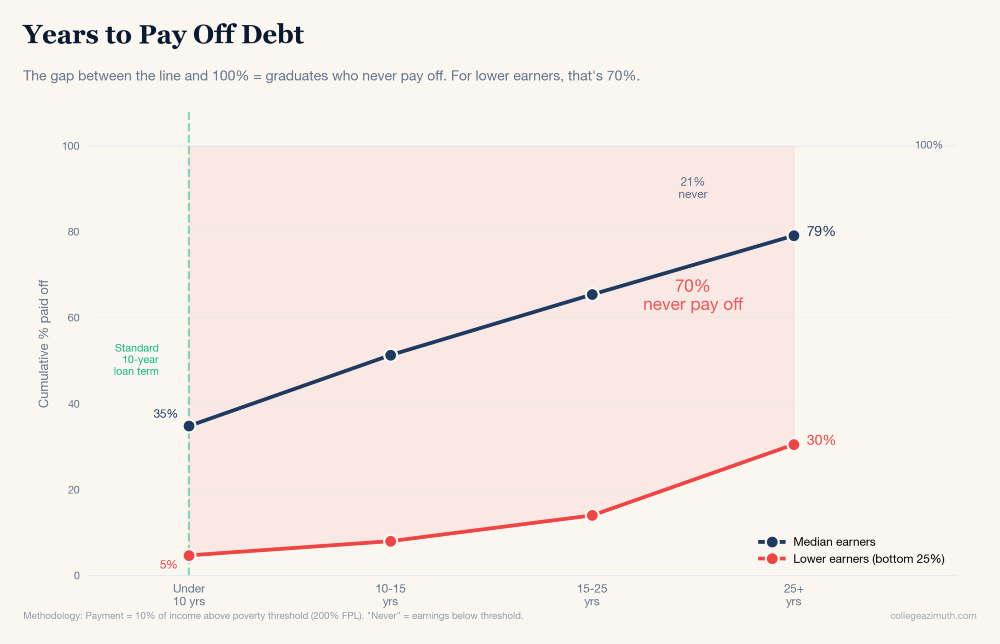

At 95% of schools, P25 graduates either have no discretionary income OR face a break-even timeline of 10+ years.

Compare that to the median: at P50, 35% of schools have break-even under 10 years. At P25? Just 4.7%.

More than 6x more schools work for median earners than for P25 earners.

Who is included in the 25th Percentile

Here's a fair question: if P25 earners are struggling, maybe they also borrowed less — so the math isn't as bad as it looks.

We checked. P25 borrowers carry an average of 5,820 dollars in debt — compared to 16,417 dollars for median borrowers. That's 64% less.

But here's what that likely reflects: P25 debt is dropout debt.

Think about who ends up at P25 earnings. It's some mix of:

The dropout: Left early. Didn't finish the degree. Accumulated less debt because they weren't there long enough to borrow more. But they also didn't get the credential — so they're stuck with debt and no degree premium. This is probably the worse place to be.

The unlucky completer: Finished the program. Accumulated the full debt load. Got the degree but landed in a low-paying job, a tough labor market, or a field that didn't pay what they expected.

The P25 debt figure (~6K) likely skews toward the first group. The median debt figure (~16K) reflects the second.

So we ran the analysis both ways:

| Scenario | What It Represents | % of Schools Where P25 Struggles |

|---|---|---|

| P25 earnings + P25 debt | Dropout scenario — less debt, no degree | 78.7% |

| P25 earnings + Median debt | Unlucky completer — full debt, low earnings | 91.9% |

Either way, the math doesn't work. The dropout has less debt but no credential. The completer has the degree but the full debt load. Both end up in the same place: P25 earnings, struggling to break even.

And here's the fundamental problem: at 70% of schools, P25 earnings are below the poverty threshold. Whether you owe 5,000 or 25,000, if your discretionary income is zero, break-even is undefined.

This Isn't a "Bad School" Problem

You might be thinking: okay, but this is probably concentrated in for-profit schools or low-quality institutions. Avoid those, and you're fine.

Here's the sector breakdown:

- For-Profit: 98% of schools have P25 struggling

- Public: 97% of schools have P25 struggling

- Private Nonprofit: 89.9% of schools have P25 struggling

Even at private nonprofits — the "best" sector by most measures — nearly 90% of schools have P25 graduates either below threshold or facing 10+ year break-even.

Where does it work? About 10% of private nonprofits and 3% of publics have P25 graduates who can actually afford their debt. These tend to be selective institutions — places where even the lower earners still make enough to have discretionary income. Flagship state universities. Well-resourced privates with strong career pipelines. See our best value colleges rankings.

And the for-profits where it works? We looked at every one. They're almost all nursing schools. Chamberlain University. West Coast University. Denver College of Nursing. A clear credential, a regulated profession, a direct job pipeline. That's the exception — not the rule.

But that's roughly 200 schools out of 4,500. For the other 95%, the math doesn't work for the bottom quarter.

This isn't something you can fix by avoiding the "wrong" schools. It's structural. It's systemic. It affects every sector.

The issue isn't which schools exist. It's how we measure and communicate ROI. When we only talk about medians, we're ignoring a quarter of the distribution.

What P25 Can and Can't Tell Us

Here's where I have to be honest about what we don't know.

Who ends up at P25?

The College Scorecard data we're using measures earnings "10 years after entry" — not after graduation. That means P25 includes some mix of:

In some cases, P25 = non-completers:

- Students who enrolled, borrowed, but didn't finish

- They have debt but not the degree premium

- At schools with high dropout rates (40%+ nationally), this is a significant factor

In other cases, P25 = completers who landed low:

- Graduates who finished but entered low-paying fields

- Graduates in geographic areas with depressed wages

- Graduates who faced tough labor market timing

We can't cleanly separate these in the data. The honest answer is: we don't know the exact composition.

But either way, 25% of entrants land there. And for them, the math doesn't work.

The Real Question

Let me bring this back to where we started.

Brooking's says "the typical college graduate breaks even by age 26 or 27." And that's true — for the median.

But "typical" means median. Half earn more, half earn less. And for the quarter who land at P25 or below, the timeline stretches to 15 years, 25 years, or never.

The data doesn't say "don't go to college." It says: don't assume the median is a promise.

If you're a counselor, a parent, a student trying to make this decision — you deserve to know what the distribution looks like, not just the middle of it.

The kind of information my Army recruiter gave me. The kind that builds trust. The kind that actually helps.

Explore the data:

- Calculate Your Real College Costs → Financial GPS

- Best Value Colleges by Earnings ROI →

- Best Nursing Colleges (Where P25 Works) →

- Our Methodology: How We Calculate Value-Added →

More in this series:

[1] Lumina Foundation uses 200% of the Federal Poverty Level as the threshold for discretionary income — the point below which a household is covering basic needs. For a single person in 2025, that's 31,300 dollars. We use this framework throughout our affordability analysis.